Money: When It Comes to Spending, Patience Pays Off

“If it is good, why can’t I have it now? Why should I have to wait?” Sound familiar? Most of us have probably used this form of reasoning to get something we want. In this age of instant gratification, the answer to this question is becoming difficult. If something is good, why should we have to wait?

When we go into a store and see something we don’t have money for, the question reverberates from the credit cards in our wallets: Can’t I have it now? It is hard to see the value of postponing certain purchases in the short term. All one can see is an evening of elegant dining, a new videocassette recorder or the beautiful clothes that can be purchased with credit cards.

There is no pain and no sacrifice — until the bills come due. Some couples become shackled to credit card debts in the tens of thousands of dollars. Even relatively minor violations of this principle of deferred gratification have penalties.

We need to remind ourselves of the value in delaying gratifications. In particular we’ll see how to overcome impulse buying by realizing some real benefits of postponing buying certain major items.

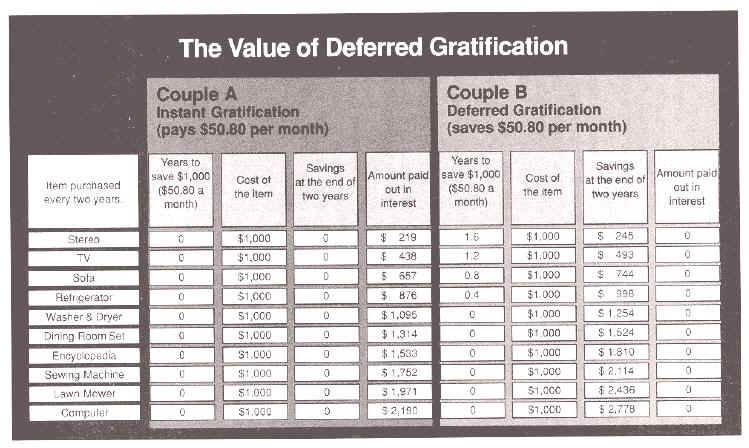

The table below contrasts instant gratification with deferred gratification. It illustrates the long-term advantages of delaying purchases over buying on credit, even when the use of credit seems relatively minor. Couple A and couple B are financially equal for this comparison. The only difference is how they handle $50.80 of their income each month over a 20-year period. They will each use their $50.80 a month to make a $1,000 purchase every two years.

Couple A buy on impulse. They use their credit card, at 19.8 percent interest, and pay it back over a two-year period. The payments on such a loan are $50.80 a month, which is how we derived this figure. Couple B defer gratification. They don’t buy the item until they have saved the money. So they save $50.80 a month until they have $1,000. Then they continue to save $50.80 a month for the remainder of the two-year period. We assume a savings interest rate of 3 percent.

At the end of the first two years, each couple makes another purchase of $1,000. Both have the first item paid off and start over. The only difference now is that couple B have savings accumulated and can wait a shorter time to buy the next item.

The chart illustrates the benefits of deferred gratification over a 20-year period. Couple B have all the same things as couple A and have to defer gratification only the first four times, with the duration diminishing each time. And couple B have a net savings of $2,778, whereas couple A have no savings — all because of how the two couples handled the same amount of money, $50.80 a month.

But this does not tell the whole story. Deferring gratification brings other benefits. We tend to think more before we buy. Those who use credit cards buy on average about 30 percent more than cash customers, which indicates compulsive buying, and buying unnecessary items.

With cash in hand, one thinks twice about the wisdom of a purchase. Having already earned the money, one more fully appreciates the value of it. Also, when paying with cash is an option, merchants will often give a cash discount. After all, credit card companies charge 3 to 5 percent to retailers just to process the charge. Sometimes the store offering the lowest price does not even take credit cards.

Proverbs contains admonitions to practice deferred gratification. “Whoever loves pleasure will suffer want; whoever loves wine and oil will not be rich” (Proverbs 21:17, New Revised Standard Version). Proverbs 21:5 adds, “The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to want.”